Source: American Airlines

American Airlines Group Inc., has reported its first-quarter 2026 financial results, including:

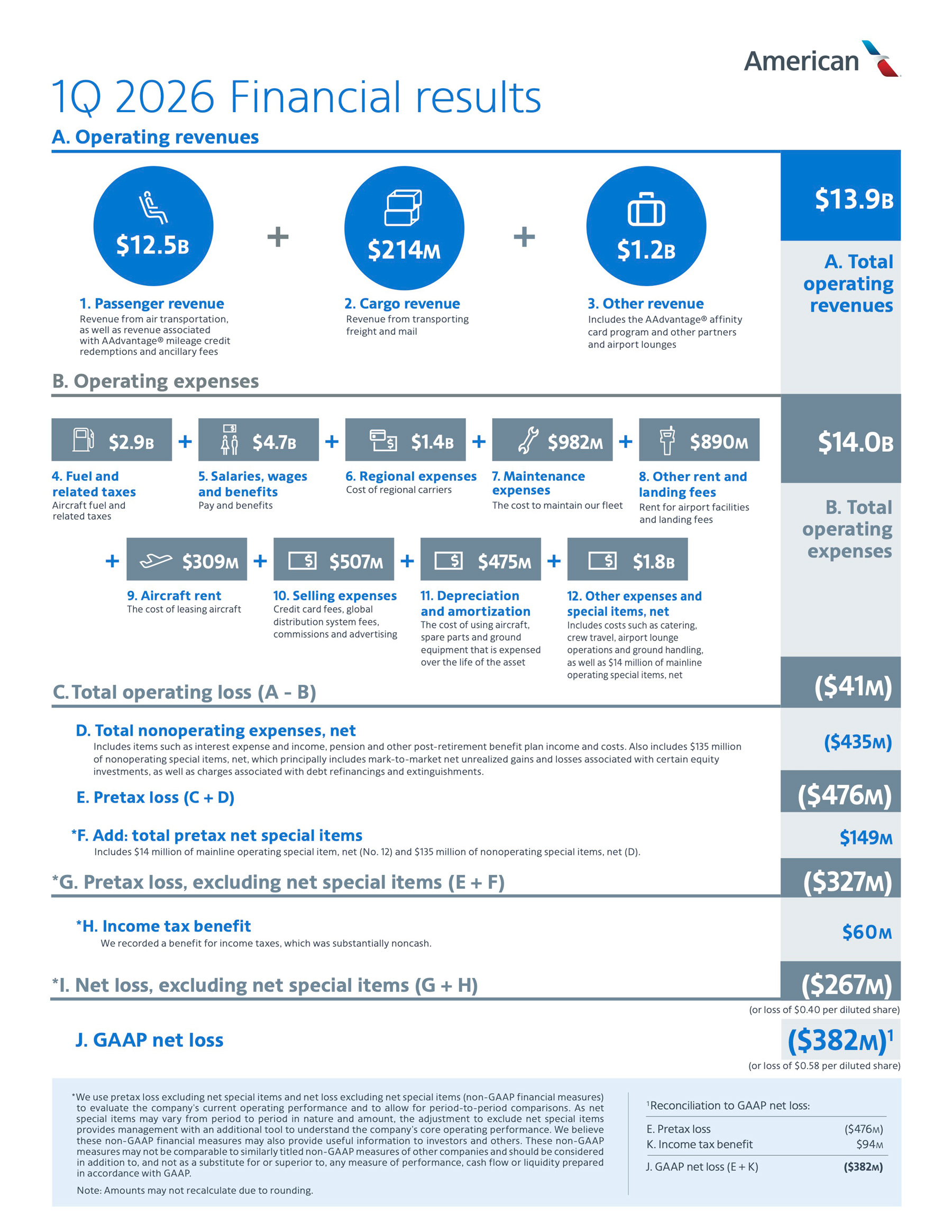

- Record first-quarter revenue of $13.9 billion

- First-quarter GAAP net loss of $382 million, or ($0.58) per diluted share

- Excluding net special items1, first-quarter net loss of $267 million, or ($0.40) per diluted share

- Ended the quarter with total debt2 of $34.7 billion, the company’s lowest total debt level since mid-20152

- Second-quarter adjusted EPS3 expected to be between ($0.20) and $0.20. Based on the forward fuel curve and the current revenue outlook, the midpoint of the full-year guidance is expected to be approximately flat to 2025, despite a greater than $4 billion increase in expense related to higher prices for jet fuel

“American delivered record revenue in the first quarter, and we’re on track for another record in the second quarter,” said American’s CEO Robert Isom. “This revenue momentum is the result of focus on our four commercial priorities — elevating the customer experience, growing our global network, driving premium revenue and leading in loyalty. Even in a volatile operating environment, our pretax margin improved by nearly 2 points year over year, and we still anticipate modest profitability for the year assuming the current forward fuel curve. Demand for our product is growing, and our customer satisfaction scores are improving. We have built a strong foundation to deliver value for our customers, team members and shareholders in 2026 and beyond.”

American’s four multiyear commercial initiatives are driving results. The company delivered record first-quarter revenue of $13.9 billion, despite an estimated $320 million revenue impact from winter storms. Demand was strong in the first quarter, and American recorded the nine highest revenue intake weeks in its 100-year history. American had year-over-year total revenue growth of 10.8% in the quarter. Total unit revenue was 7.6% higher year over year, improving sequentially each month in the quarter, culminating with March domestic and international passenger unit revenue both up more than 10% year over year. American’s domestic, Pacific and Atlantic entities delivered positive unit revenue growth year over year, with Atlantic passenger unit revenue up 16.7%. Demand remains strong, and based on current bookings, American expects total revenue growth between 13.5% and 16.5% in the second quarter.

Elevate the customer experience

American continues to elevate every step of the customer travel journey. The company offers the industry’s most extensive premium lounge network and is making significant investments in its Flagship® and Admirals Club® lounges at Chicago O’Hare International Airport (ORD), Miami International Airport (MIA), Charlotte Douglas International Airport (CLT), Ronald Reagan Washington National Airport (DCA), Austin-Bergstrom International Airport (AUS) and Nashville International Airport (BNA).

American is increasing the number of premium seats across its fleet through new deliveries and retrofits. In the first quarter, lie-flat and Premium Economy seats grew more than twice as fast as Main Cabin seats. In addition, the company has improved connectivity and elevated the inflight experience, successfully rolling out free high-speed satellite Wi-Fi, sponsored by AT&T, for AAdvantage® members in January. The airline now offers free high-speed satellite Wi-Fi on more aircraft than any other carrier globally. Additionally, American introduced new features in its digital app that provide transparent, real-time notifications and more self-service options for customers to independently manage their itineraries in one convenient location.

American invested in strengthening its schedules across the system and rebanking its operation at Dallas Fort Worth International Airport (DFW) to reinforce operational reliability, ensuring customers experience more on-time flights and an overall smoother travel experience at its largest and most impactful hub. The company is also rebanking its operation at Philadelphia International Airport (PHL) to a seven-bank structure to grow and improve trans-Atlantic connectivity.

Grow the global network

American operates the strongest domestic network in the industry and is prioritizing scaling local share in its hubs by utilizing existing infrastructure, particularly in Philadelphia, Miami and Phoenix. American supports the FAA’s action to establish an operational framework in Chicago that will benefit all customers. This summer, American expects to operate approximately 500 flights per day in Chicago, all featuring high-speed satellite Wi-Fi and premium cabins.

The company recently announced a multiyear investment in Concourse D in Miami, which is expected to enhance American’s leading Latin America franchise with improved operations, elevated customer experience and more convenient international travel. American’s network, combined with the global reach of its joint business and oneworld partners, connects more people to more places than any other airline.

Drive premium revenue

American remains focused on increasing premium, high-margin revenue. The company continued to win share in corporate channels during the first quarter, with managed corporate revenue increasing 13% year over year. Additionally, American is focused on increasing premium leisure revenue and improving upsell to higher-margin products. Premium unit revenue continued to outperform the Main Cabin in the first quarter.

Lead in loyalty

American’s AAdvantage® program is the largest airline loyalty program, offering the highest value per mile of any airline in the U.S., numerous ways to earn and redeem miles and greater opportunities for member engagement. The AAdvantage® program continues to evolve and resonate with customers, as evidenced by record enrollments in the first quarter, up 25% year over year.

At the beginning of the first quarter, American’s exclusive and expanded co-branded credit card partnership with Citi took effect. During the quarter, the company achieved record acquisitions and co-branded credit card spend was up 9% year over year.

Balance sheet and liquidity

The company has made significant progress on its financial priorities, ending the quarter with total debt2 of $34.7 billion, the first time it has been below $35 billion since mid-20152. The company finished the quarter with $10.8 billion in liquidity and more than $27 billion in unencumbered assets and first-lien borrowing capacity. This strong financial position provides significant flexibility in the current environment.

Financial guidance

The company’s second-quarter 2026 guidance assumes continued revenue improvement in the domestic entity, growth in corporate customer volumes and the ability to partially recapture elevated fuel prices, currently assumed to be approximately $4.00 per gallon. Based on the forward fuel curve and the current revenue outlook, the midpoint of the company’s full-year earnings guidance is approximately flat to 2025, despite a more than $4 billion increase in expense related to higher prices for jet fuel.

| Adjusted earnings (loss) per diluted share3 | ($0.40) to $1.10 |

| Available seat miles (ASMs) | Up 4.0% to 6.0% |

| Total revenue | Up 13.5% to 16.5% |

| CASM excluding net special items, fuel and profit sharing4 | Up 2.0% to 4.0% |

| Adjusted earnings (loss) per diluted share3 | ($0.20) to $0.20 |

Notes

See the accompanying notes in the financial tables section of this press release for further explanation, including reconciliations of certain GAAP to non-GAAP financial information.

- The company recognized $115 million of net special items in the first quarter after the effect of taxes.

- All references to total debt include debt, finance and operating lease liabilities and pension obligations. 2015 total debt includes pro forma lease liabilities.

- Adjusted earnings (loss) per diluted share guidance excludes the impact of net special items and represents an absolute number, not a year over year comparison. The company is unable to reconcile certain forward-looking information to GAAP as the nature or amount of net special items cannot be determined at this time.

- Cost per available seat mile (CASM) excluding net special items, fuel and profit sharing is a non-GAAP measure. The company is unable to reconcile certain forward-looking information to GAAP as the nature or amount of net special items cannot be determined at this time.

Financial results

To download the first-quarter 2026 financial results click here: View the PDF